Business Rates and the £300m Pub Relief: The Reality of Hospitality Businesses in 2026

Written by Stu Dawson

A “£300 million pub relief package” dominated headlines in the run-up to Chancellor Rachel Reeves’s announcement on 27 January 2026. Whilst she confirmed relief for pubs and live music venues, realistic estimates place the first-year cost at around £80 million for 2026-27, reflecting a 15% business rates discount. The move followed months of sector pressure after the November 2025 Autumn Budget revealed significant business rates increases, prompting a lot of pub owners to bar Labour MPs in protest.

This relief offers qualifying venues a discount on their business rates bills, applied after existing reliefs. However, the package also highlights a clear divide within hospitality, as restaurants, cafes, and hotels that face similar (and in some cases steeper) cost pressures are excluded. More fundamentally, the relief tackles only one element of broader cost challenges, including rising wages, supplier inflation, and weakened consumer confidence.

This article examines the current business rates landscape for hospitality, what’s driving the cash flow crisis in hospitality, what the relief actually delivers, where its limitations lie, and why access to appropriate finance has become increasingly necessary for hospitality businesses in 2026.

Understanding Business Rates in Hospitality

Business rates are essentially a tax on non-domestic properties used for commercial activities. The tax is calculated by multiplying a property’s “rateable value” (an estimate of its annual rental value) by a “multiplier” set by the government.

How Hospitality is Valued Differently

For hospitality businesses, rateable values are set by the Valuation Office Agency (VOA) using a method known as fair maintainable trade/turnover (FMT). Simply put, this method reflects the level of turnover a reasonably efficient operator could expect to achieve when handling a specified business. This is fundamentally different from most commercial properties, which are valued on rental evidence. For pubs, restaurants, and hotels, the VOA analyses trading turnover during revaluations, then applies industry-agreed percentages to convert that turnover into a rateable value.

April 2026 Revaluation Are Higher

Revaluations take place every three years. This year’s revaluation (happening in April) would be based on trading evidence from April 2024. That time is significant because in 2024, much of the sector had recovered from the pandemic, with many venues trading at or above pre-Covid levels. In contrast, the 2023 revaluation was based on April 2021, when lockdowns and restrictions were still heavily affecting turnover. That shift in valuation dates goes a long way towards explaining the scale of recent business rate spikes with VOA top officials confirming that some pubs face as high as 100% increase in the ratable value when compared to last valuation.

Support Mechanisms: What Exists and What’s Changed

For many SME hospitality businesses, these revaluation increases translate into higher bills. For example, an independent pub with a rateable value increasing from £35,000 to £50,000 would see its annual rates bill jump from about £10,479 to £12,051 despite existing reliefs.

To understand how businesses are being supported (and where support falls short), it’s worth examining the mechanisms now in place

Small Business Rates Relief (SBRR)

Properties with rateable values of £12,000 or less receive 100% relief, meaning they pay no business rates. Relief then tapers from 100% to 0% for properties valued between £12,001 and £15,000. These thresholds remain unchanged going into the 2026-27 financial year.

Transitional Relief

To cushion businesses from sudden bill increases following VOA revaluation, the new budget for 2026 caps year-on-year increases at:

- £20,000 (£28,000 in London): 5% cap in 2026-27

- £20,001 to £100,000: 15% cap in 2026-27

- Over £100,000: 30% cap in 2026-27

These caps increase in subsequent years (with inflation added), but provide immediate protection against revaluation shock.

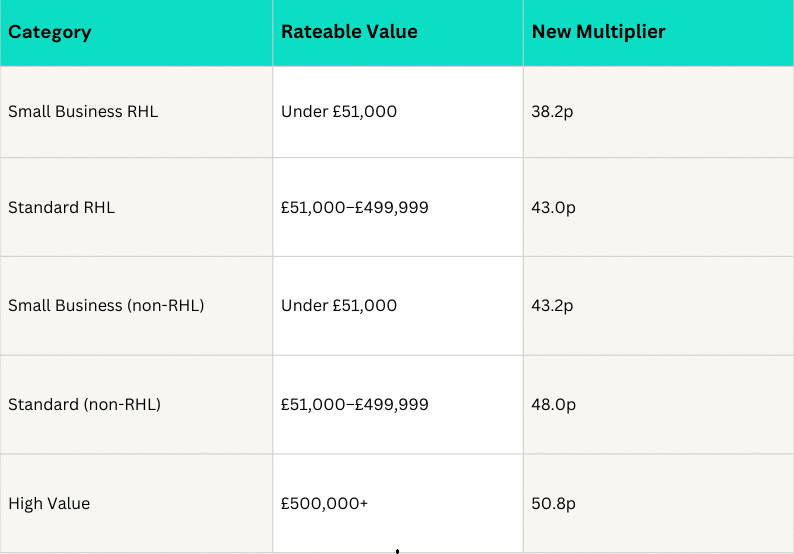

Permanent Multipliers (Major 2026 Change)

The November 2025 Budget replaced the temporary 40% Retail, Hospitality and Leisure (RHL) relief (originally introduced as COVID emergency support) with a new permanent structure of lower multipliers

For many SME hospitality businesses, the 12p multiplier reduction cannot offset both the loss of 40% relief and dramatic valuation increases.

Despite These Measures, Bills Still Rise Substantially

On paper, the November 2025 Budget sounded positive: permanently lower multipliers funded by higher rates on large distribution warehouses, delivering a £900 million annual tax cut for over 750,000 RHL properties. However, for many SME hospitality businesses, the 12p multiplier reduction cannot offset both the loss of 40% relief and dramatic valuation increases.

The business rates challenge is compounded by other costs hitting simultaneously in 2026:

- National Living Wage rising to £12.71

- Alcohol duty up 3.66%, directly impacting wet sales margins (this started in February)

The cash flow backdrop remains fragile. Research from UKHospitality suggests 29% of hospitality operators hold no cash reserves, while 73% have less than six months’ cover. With several fixed costs rising in April, just as venues require working capital to prepare for peak spring and summer trading, the timing creates a clear liquidity squeeze.

All of this sits against softer consumer demand. Frozen income tax thresholds continue to weigh on discretionary spending, which hospitality depends on almost entirely. At the same time, structural shifts such as hybrid working reducing weekday city centre footfall, and younger demographics consuming less alcohol, are reshaping traditional pub and restaurant models.

What the Package Delivers, Who Qualifies, and Who Doesn’t

The additional relief announced on 27 January 2026 offers qualifying venues a 15% discount on their business rates bills, applied after existing transitional reliefs and reduced multipliers. The government estimates this will save the average pub approximately £1,650 in 2026-27.

This figure is based on an illustrative calculation: a pub with a rateable value rising from £30,000 to £39,000 would have a base bill of £14,898. Supporting Small Business relief caps the increase at £10,329, then the 15% relief brings the final bill to £8,780, a saving of approximately £1,650.

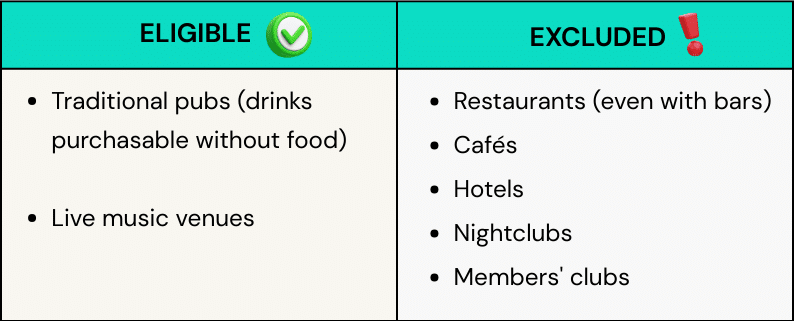

However, eligibility is more restrictive than many expected. The relief applies to pubs where customers can purchase drinks without being required to order food and live music venues. Local authorities determine eligibility on a case-by-case basis, considering factors such as whether the premises demonstrate pub characteristics in operation and licensing. Critically excluded are restaurants (even those with bars), cafés, hotels, nightclubs, and members’ clubs where public access is restricted.

This decision created a stark divide within the sector. Hotels face particularly severe increases: the average hotel’s business rates bill is projected to rise by £28,900 in 2026-27 alone, reaching a cumulative £205,200 over three years, a 115% increase. Restaurants and cafés occupy an uncomfortable middle ground, operating with business models similar to pubs yet explicitly excluded. The requirement that customers must be able to purchase drinks without food bars them from relief, despite many restaurants diversifying their offerings to adapt to changing consumer preferences and hybrid working patterns.

Relief or Not: The Universal Cash Flow Challenge

The average £1,650 saving for qualifying pubs and live music venues is welcome, but it does not materially change the financial reality facing much of the sector. Across England and Wales, an average of one pub closed every day in 2025. That alone suggests the strain runs deeper than a single line of relief.

Whether a hospitality business qualifies for the additional 15% pub relief or not, the core cash flow challenge remains largely unchanged. Hospitality trading is inherently seasonal. Revenue rises and falls throughout the year, yet wages, rent, utilities and supplier payments continue regardless.

April 2026 brings a concentration of pressure points, including higher employment costs, revised rates and other fixed overhead increases, all landing at once and irrespective of trading performance. With a significant proportion of operators reporting limited or no cash reserves, many businesses face immediate liquidity gaps rather than long-term profitability issues.

In that environment, the conversation shifts from cost savings to cash timing. For many operators, the question is not whether they are viable, but how to bridge short-term gaps without damaging long-term stability. That is where structured, short-term financing solutions become a practical tool, helping businesses manage seasonal volatility and meet fixed obligations without placing additional strain on already stretched reserves.

Working Capital That Aligns with Trading Patterns

Whether a business qualifies for this relief or not, the priority should be working capital that supports trading rather than adding to fixed strain. Revenue-based finance, such as a Merchant Cash Advance, is designed around that reality. It provides funding against future card sales and does not require fixed monthly repayment schedules. Instead, repayments move in line with card sales. This means that when trade slows, repayments reduce. When trade strengthens, the balance clears faster, without penalties for early settlement.

Businesses that address working capital needs before reserves are exhausted retain more control. While those operating with no reserves face immediate liquidity pressure, making access to flexible, revenue-aligned funding, essential. In a sector like this, proactive funding decisions shouldn’t only be about growth ambition. They should also be about stability, continuity and giving otherwise sound businesses the breathing space to trade through sustained pressure.

365 Finance provides revenue-based funding for hospitality and retail businesses processing card payments. Flexible repayments linked to trading performance support businesses through timing gaps without the pressure of fixed monthly obligations. For businesses facing April’s rates spike or seasonal cash flow pressure, exploring flexible funding aligned with trading patterns may provide the breathing room needed to navigate what remains a structurally challenging environment.

Speak with your broker or contact 365 Finance directly to explore whether revenue-based funding could support your operational cash flow planning.