5 Smart Ways to Raise Money for Your Business

Written by Team 365 Finance

Running a small business in the UK means managing constant pressure. Tight margins. Seasonal fluctuations. Unexpected equipment failures. Supplier terms that clash with payroll dates. Policy changes that reshape cost bases, from business rates to new lending regulations. It’s within this reality that critical business decisions get made, day in and day out. Decisions about expansion. Decisions about closing cash flow gaps, managing stock levels without depleting reserves, or seizing time-sensitive opportunities before they vanish.

Having the funds available when needed rarely aligns with the pace at which these decisions must be made. Traditional funding sources, particularly bank loans, remain structured for a different business environment entirely: one with longer timelines, extensive documentation requirements, and a risk appetite that often excludes the very businesses that drive the UK economy.

This guide offers a different approach. Rather than presenting one “best” option, it breaks down five realistic ways businesses, especially SMEs, raise money, when each works well, and when it doesn’t. The goal: informed decisions made on the business’s terms, not under pressure.

Understanding Business Funding Beyond the Crisis Narrative

Access to capital is often framed as a last resort; something businesses turn to when cash runs out or an unexpected bill arises. But this characterisation is incomplete and misses the bigger picture. For many businesses, the right funding at the right time isn’t a safety net. It’s a practical tool that enables them to act when opportunities arise, rather than letting them pass by.

Consider a restaurant owner who secures working capital ahead of peak season. They can take on more staff, invest in marketing, and manage stock levels without the constant pressure of juggling outgoings week to week. These aren’t extraordinary scenarios. They reflect the difference between running a business reactively and running one with intent.

This Matters Especially for SMEs

If you run a salon, a restaurant, a trade business, or a retail shop, the numbers reflect a familiar reality. Recent research shows that 81% of SME owners say a lack of finance prevented them from pursuing growth opportunities in 2025. In other words, four out of five businesses missed real opportunities because the capital wasn’t available when it was needed.

At the same time, 90% of UK businesses are now facing payment delays, according to Coface, with the average small business owed over £21,000 in unpaid invoices (QuickBooks). This means work has been completed and invoices issued, yet cash flow remains uncertain while rent, payroll, and supplier bills continue on schedule.

What to Consider Before Choosing a Funding Option

-

How Revenue Flows Through the Business

The funding structure needs to match how cash actually moves through the business. Revenue model determines which funding options are structurally accessible. Businesses that take card payments (restaurants, salons, retail, auto services) have consistent, verifiable transaction records that many lenders can assess and work with directly. Businesses that invoice on terms such as agencies, contractors, B2B providers, may find invoice finance a more natural fit than traditional loans. Seasonal businesses often struggle with fixed monthly repayments during slower periods, regardless of the rate attached.

-

Speed vs. Cost

Funding that arrives in days typically costs more than funding that takes weeks. This is the price of immediacy. Whether the trade-off is worthwhile depends on what the capital enables. Time-sensitive opportunities, such as bulk stock purchases, revenue-generating equipment, or seasonal demand, may justify higher costs if the alternative is missed revenue.

-

Credit History and Trading Record

Strong credit expands available options and improves terms. Less-than-perfect credit narrows the field and increases costs, but it does not remove access entirely. Several viable routes remain available to SMEs without pristine records. This guide covers both ends of the spectrum.

The Smartest Funding Options for SMEs

-

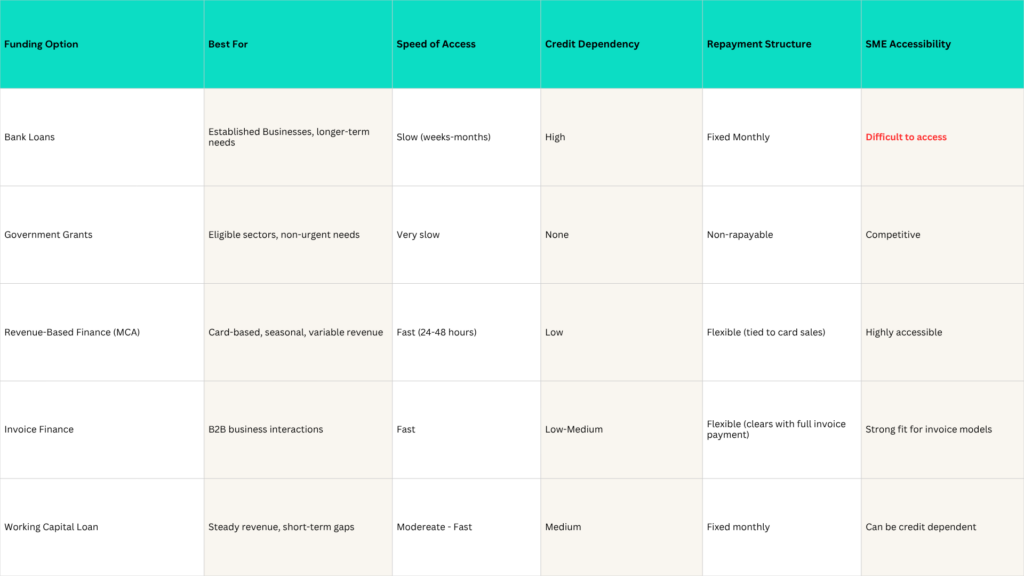

Bank Loans

Bank loans are the most familiar form of business funding for owners and operators. They are often seen as the default option when external finance is needed. A traditional bank loan provides a lump sum repaid over a fixed term with monthly instalments.

For businesses with strong financials and solid credit profiles, it is one of the lowest-cost forms of borrowing. However, its limitations are well documented for SMEs. For instance, approval processes are slow, often taking weeks or months. Collateral or personal guarantees are common, and rejection rates for smaller businesses are significant.

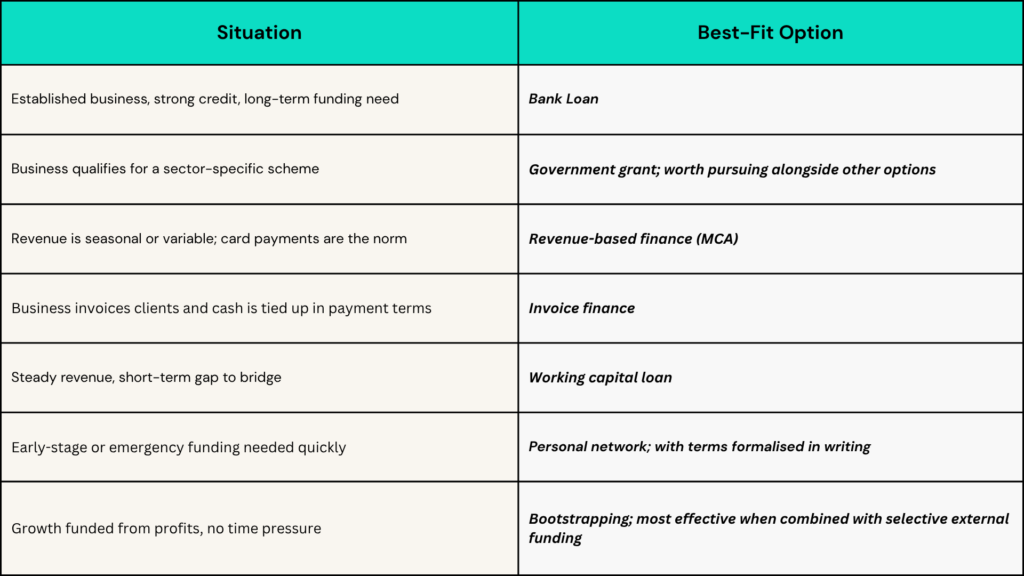

Therefore, for businesses in the early years, or those with fluctuating revenue or less-than-perfect credit, a bank loan is often the first option explored and the first ruled out. It is worth considering, but having a plan B from the outset is essential.

-

Government Grants and Support Schemes

Government grants are non-repayable funding, which makes them immediately attractive. The reality is that they are highly competitive, often sector-specific, and rarely straightforward to apply for. Schemes like Innovate UK, the UK Shared Prosperity Fund, and various local enterprise partnership programmes can offer meaningful support, but the application process is time-intensive and approval is far from guaranteed. Grants work best as a supplementary strategy, not a primary funding source.

-

Revenue-Based Finance (Merchant Cash Advance)

A Merchant Cash Advance funding provided against future sales. Instead of repaying a fixed loan amount each month, the business receives an advance on future revenue and repays it through a small percentage taken from daily card transactions until a pre-agreed total is settled.

This structure reflects how many businesses actually earn. For instance, a restaurant does not generate the same revenue year-round. A salon’s busiest periods shift across the calendar. Revenue-based repayments adjust accordingly as collections rise and fall with trading activity.

Why it works for smaller and newer businesses

- No need for significant collateral or perfect credit

- Eligibility based primarily on card sales and trading history

- Fast decisions, often within 24 – 48 hours

Note: Revenue-based finance is typically more expensive than a traditional bank loan. But for businesses operating on tight timelines, the cost of missing an opportunity because funding arrived too late (or not at all) is often far greater than the difference in price.

-

Invoice Finance

Invoice finance allows businesses to unlock cash tied up in unpaid invoices. Rather than waiting 30, 60, or 90 days for a client to pay, a lender advances a percentage of the invoice value upfront (typically 70-90%), with the balance paid once the customer settles. Two structures exist: invoice factoring, where the lender manages credit control and collections on your behalf, and invoice discounting, where you retain control and the arrangement remains confidential.

For B2B businesses that invoice on payment terms, such as agencies, contractors, consultancies, and trade suppliers, this can be a highly effective cash flow tool. It turns the gap between completing work and receiving payment into something manageable, while reducing the burden of chasing late payments.

This only works if your business raises invoices to customers. For restaurants, salons, retail shops, or any business paid at the point of sale, traditional invoice finance does not apply. That said, some lenders offer related structures (such as purchase order finance) that can help fund large supplier orders or bulk stock purchases, though these are less common and typically reserved for established trading relationships with verified purchase orders.

-

Working Capital Loans

Working capital loans are short-term borrowing designed to cover the operational costs of running a business (stock, wages, utilities, rent) rather than long-term investments. They bridge the gap between money going out and money coming in.

Traditionally, working capital loans from alternative lenders are faster to access than bank loans and more flexible on credit criteria. However, they might come with monthly repayments. Luckily, not all working capital finance is structured this way.

Some unsecured business loans operate on the same revenue-based repayment model as a Merchant Cash Advance in which repayments are collected as a percentage of daily card sales, so they adjust automatically with trading performance. There are no fixed terms, no interest rates or APRs, and no collateral required.

Honourable Mentions

-

Personal Networks (Friends, Family, and Business Contacts)

Personal networks can be a practical source of informal funding, particularly in early stages or genuine emergencies. Risks still exist, mixing personal relationships with financial obligations can cause strain if expectations are not clearly agreed upfront. If this route is used, treat it with the same formality as any other financial arrangement.

-

Bootstrapping (Self-Funding Growth)

Reinvesting profits and funding growth from trading activity is the default for many business owners, and there is nothing wrong with it. It preserves ownership and enforces discipline. The trade-off is speed. A competitor secures the prime location. A supplier relationship goes to someone who could buy in volume. A seasonal window closes before stock arrives. For most SMEs with real growth ambitions, bootstrapping works best in combination with strategic external funding, not as the only tool available.

Choosing the Right Option for Your Business

The Right Funding Fits the Way Your Business Runs

The funding landscape has shifted. Traditional bank lending was built for a different era; one with longer timelines, predictable revenues, and a risk appetite that suited a different kind of business. Most businesses today operate with cash flow that moves unevenly, costs that shift without warning, and opportunities that do not wait for a credit committee.

That is why more businesses are moving towards funding structured around how they actually trade, not how a lender prefers them to. There is no single right answer across the five options covered here. The right one depends on your revenue model, your timeframe, and what you are trying to achieve. What this guide should make clear is that the options are wider than most business owners assume, and that a rejection from a bank is a starting point, not a full stop.

365 Finance provides revenue-based funding for businesses processing card payments, from hospitality and retail to salons, trades, and service businesses. Flexible repayments linked to trading performance support businesses through cash flow gaps without the pressure of fixed monthly obligations. Whether the need is seasonal, structural, or time-sensitive, exploring flexible funding aligned with how your business actually earns may provide the breathing room needed to keep moving forward.